Inorganic Activity is Inevitable in The Domestic Airline Business, given The Huge Overdues, debt load and losses. The Skies are open for Consolidation and pe activity. Sellouts or mergers – what will happen?

The big takeaway from mergers in the world’s largest airline market (US) is that this practice of buying and selling in this business does not fit into profitable categories in an unhealthy environment. Instead, the converse happens. US Airways tied the knot with AmericaWest in 2005. Then, both were making losses. And the sector had just lost $37.4 billion during the past four years globally. For five years post-merger, the two accumulated $12.1 billion in losses. Strangely, last year, the combine returned to profitability ($502 million; a time when globally, the industry recorded $18 billion in profits). Another big-ticket marriage was the Delta-Northwest merger of April 2008. Between 2001 & 2006, the two airlines had recorded a total loss of $33.1 billion, filed for bankruptcy and emerged a leaner machine. During the year that preceded the merger, the two had reported a combined positive bottomline of $3.93 billion. The sector too was happier, with global profits of $19.7 billion in FY2006 & 2007. Both imagined that the time was right – it was a merger of two profit-making airlines! What followed was unexpected. Between 2008 and 2009, the merged entity lost $10.2 billion (the sector lost $25.9 billion). As in the case of the newly merged US Airways, the new Delta made $593 million in profits in FY2010. You could draw up umpteen similarities between the cases mentioned above, but the two most important – which most ordinarily miss – are: first, the airlines were allowed to fail, file for Chapter 11 and then given a shot at another day; and second, both bled when the North American airline market bled. Both made merry when the sector made cash (in FY2010, US airlines made profits of $4.1 billion).

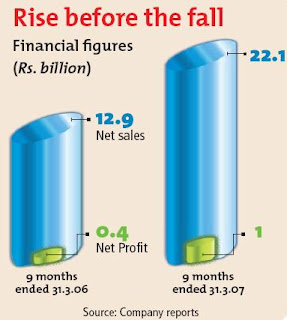

Guardians in the Indian airline space didn’t quite understand this. They still don’t. Be it the Jet-Sahara deal or the Kingfisher-Deccan acquisition or the merger of Air India and Indian, it all happened during a time when every party involved carried the “loss-maker” tag. More importantly, it occurred in a bleeding sector. M&As don’t work every time. That is known. They never work in a loss-making industry. This is what the Indian aviators forgot. Today, these three merged entities (which command 60.2% of the domestic market; DGCA data for June 2011) are in the middle of a bloodbath. They live in an environment, which domestically has been a kitchen sink for the past six years. Last year, Indian aviators lost a total of $400 million; ironically, the global aggregate was a positive $18 billion! While Jet lost Rs.858.4 million, Kingfisher lost Rs.10.27 billion and Air India more than Rs.57 billion. What is the cure?

Overcrowding is a concern. It implies suffocation for all. Currently, there are six groups in the Indian market. This as per market experts, is one too many. With a domestic passenger count of 52 million a year, a merger or a sell-out over the next two years is expected. While speaking to B&E from Manchester, Gordan Bevan, VP - Consultancy Services for Airport Strategy & Marketing, UBM Aviation Worldwide, opines, “An expanding economy such as India’s does not need four national carriers, all specialising on a hub and spoke legacy business model, with all four hubbing through either Delhi or Mumbai, both of which have capacity constraints. As an example, the growth of the airline industry in newly-liberalised Eastern Europe did not result in the creation of more large carriers.” There you have the exact count – we need four big FSC/LCC groups to have a healthy competitive environment given the footfalls.

And what in the case of a takeover? Which is the most-likely target? Let us look at the two biggest current issues ailing the Indian aviators besides the unhealthy fare war. First, ATF prices, which soared by 51% y-o-y during H2, FY2010-11. To understand how airlines suffer, Jet shelled out an additional Rs.4.43 billion on fuel during Q4, FY2010-11 resulting in a loss for the year. So who suffers due to fuel cost rising up to 39% of operating cost during the quarter ended June 30, 2011? Ketki Mahajan, Aerospace Analyst at Frost & Sullivan, shares her view with B&E. “Airlines can no longer work on the LCC model. This is because of high crude prices, and high ATF tax levied by various states, high airport charges and rising service tax on fares.” This brings us to the next problem: taxes. Sudheer Raghavan, COO, Jet Airways, tells B&E that at times, the tax issue makes him wonder “why Jet is in the airline business at all.” Therefore, under such a circumstance where airlines are paying 33.5% more than what they were doing 12 months back on fuel (due to rise in ATF tax), life for LCCs becomes difficult. Actually, impossible. All indicators therefore point to the smallest of the LCCs being up for grabs – GoAir, with a fleet of 10 A320s and a 6.1% market share (June 2011). In fact, CAPA has even forecasted that GoAir could exit the market through a sell-out, as Singapore-based Binit Somaia, CAPA’s APAC Regional Director tells B&E, “Given the size of the Indian market today, it has a large number of airlines operating, with limited differentiation in their networks and models. There does exist therefore the potential for some further consolidation.” But suitors would want to woo GoAir before 2015, as the year would see it add another 78 A320s to its fleet, thereby increasing the airline valuation multi-fold. If GoAir has to go, it will be best bought by another airline, any time after March 2012 (Indian carriers are forecasted to register their first profit in 7 years, of anywhere up to $400 million in FY2012, as per CAPA).

Guardians in the Indian airline space didn’t quite understand this. They still don’t. Be it the Jet-Sahara deal or the Kingfisher-Deccan acquisition or the merger of Air India and Indian, it all happened during a time when every party involved carried the “loss-maker” tag. More importantly, it occurred in a bleeding sector. M&As don’t work every time. That is known. They never work in a loss-making industry. This is what the Indian aviators forgot. Today, these three merged entities (which command 60.2% of the domestic market; DGCA data for June 2011) are in the middle of a bloodbath. They live in an environment, which domestically has been a kitchen sink for the past six years. Last year, Indian aviators lost a total of $400 million; ironically, the global aggregate was a positive $18 billion! While Jet lost Rs.858.4 million, Kingfisher lost Rs.10.27 billion and Air India more than Rs.57 billion. What is the cure?

Overcrowding is a concern. It implies suffocation for all. Currently, there are six groups in the Indian market. This as per market experts, is one too many. With a domestic passenger count of 52 million a year, a merger or a sell-out over the next two years is expected. While speaking to B&E from Manchester, Gordan Bevan, VP - Consultancy Services for Airport Strategy & Marketing, UBM Aviation Worldwide, opines, “An expanding economy such as India’s does not need four national carriers, all specialising on a hub and spoke legacy business model, with all four hubbing through either Delhi or Mumbai, both of which have capacity constraints. As an example, the growth of the airline industry in newly-liberalised Eastern Europe did not result in the creation of more large carriers.” There you have the exact count – we need four big FSC/LCC groups to have a healthy competitive environment given the footfalls.

And what in the case of a takeover? Which is the most-likely target? Let us look at the two biggest current issues ailing the Indian aviators besides the unhealthy fare war. First, ATF prices, which soared by 51% y-o-y during H2, FY2010-11. To understand how airlines suffer, Jet shelled out an additional Rs.4.43 billion on fuel during Q4, FY2010-11 resulting in a loss for the year. So who suffers due to fuel cost rising up to 39% of operating cost during the quarter ended June 30, 2011? Ketki Mahajan, Aerospace Analyst at Frost & Sullivan, shares her view with B&E. “Airlines can no longer work on the LCC model. This is because of high crude prices, and high ATF tax levied by various states, high airport charges and rising service tax on fares.” This brings us to the next problem: taxes. Sudheer Raghavan, COO, Jet Airways, tells B&E that at times, the tax issue makes him wonder “why Jet is in the airline business at all.” Therefore, under such a circumstance where airlines are paying 33.5% more than what they were doing 12 months back on fuel (due to rise in ATF tax), life for LCCs becomes difficult. Actually, impossible. All indicators therefore point to the smallest of the LCCs being up for grabs – GoAir, with a fleet of 10 A320s and a 6.1% market share (June 2011). In fact, CAPA has even forecasted that GoAir could exit the market through a sell-out, as Singapore-based Binit Somaia, CAPA’s APAC Regional Director tells B&E, “Given the size of the Indian market today, it has a large number of airlines operating, with limited differentiation in their networks and models. There does exist therefore the potential for some further consolidation.” But suitors would want to woo GoAir before 2015, as the year would see it add another 78 A320s to its fleet, thereby increasing the airline valuation multi-fold. If GoAir has to go, it will be best bought by another airline, any time after March 2012 (Indian carriers are forecasted to register their first profit in 7 years, of anywhere up to $400 million in FY2012, as per CAPA).

Source : IIPM Editorial, 2012.

An Initiative of IIPM, Malay Chaudhuri

and Arindam Chaudhuri (Renowned Management Guru and Economist).

For More IIPM Info, Visit below mentioned IIPM articles.

IIPM Best B School India

Management Guru Arindam Chaudhuri

Rajita Chaudhuri-The New Age Woman

IIPM's Management Consulting Arm-Planman Consulting

IIPM Prof. Arindam Chaudhuri on Internet Hooliganism

Arindam Chaudhuri: We need Hazare's leadership

Professor Arindam Chaudhuri - A Man For The Society....

IIPM: Indian Institute of Planning and Management

An Initiative of IIPM, Malay Chaudhuri

and Arindam Chaudhuri (Renowned Management Guru and Economist).

For More IIPM Info, Visit below mentioned IIPM articles.

IIPM Best B School India

Management Guru Arindam Chaudhuri

Rajita Chaudhuri-The New Age Woman

IIPM's Management Consulting Arm-Planman Consulting

IIPM Prof. Arindam Chaudhuri on Internet Hooliganism

Arindam Chaudhuri: We need Hazare's leadership

Professor Arindam Chaudhuri - A Man For The Society....

IIPM: Indian Institute of Planning and Management